(2026 Breakdown)

Ask most people what it costs to buy a house and they'll quote you the asking price. But the asking price is only the beginning. Between the deposit, stamp duty, solicitor fees, surveys and moving costs, the true upfront cost of buying a home in the UK typically runs £30,000 - £50,000 on an average-priced property, and much of it has to be paid before you've even picked up the keys.

This guide breaks down every cost, line by line, with real 2026 figures, so you can budget properly and avoid the nasty surprises that derail so many purchases.

The quick answer

For the average UK home (around £270,000 in 2026, according to the ONS House Price Index), here's roughly what a buyer moving home can expect to pay upfront:

| Cost | Typical amount |

|---|---|

| Deposit (10%) | £27,000 |

| Stamp duty (home mover, England) | £3,500 |

| Solicitor/conveyancing fees | £1,000–£2,000 |

| Survey | £400–£1,500 |

| Mortgage fees | £0–£1,500 |

| Removals and moving costs | £500–£1,500 |

| Total upfront | ~£32,500–£37,000 |

First-time buyers fare better on stamp duty (often paying nothing at all), but the deposit remains the mountain. Let's take each cost in turn.

1. The deposit: the big one

Your deposit is the largest single upfront cost by far. Most lenders require a minimum of 5% of the purchase price, but the sweet spot is 10% or more - bigger deposits unlock meaningfully lower mortgage rates.

On a £270,000 home:

- 5% deposit: £13,500

- 10% deposit: £27,000

- 15% deposit: £40,500

A word of caution on the 5% route: while it gets you on the ladder sooner, you'll pay a higher interest rate for the life of the initial deal, and you're more exposed to negative equity if prices dip. If you can stretch from 5% to 10%, the monthly savings usually justify the wait.

Regional reality check: the average masks huge variation. A 10% deposit is around £51,000 in London but closer to £16,000 in the North East. In Wales, where the average home costs around £212,000, a 10% deposit is roughly £21,200.

2. Stamp duty: the tax most buyers underestimate

Stamp Duty Land Tax (SDLT) applies in England and Northern Ireland, and the thresholds tightened significantly in April 2025 - catching out buyers who remember the more generous rules. As of 2026, the rates are:

Home movers (England & Northern Ireland):

- 0% on the first £125,000

- 2% on the portion from £125,001 to £250,000

- 5% on the portion from £250,001 to £925,000

- 10% from £925,001 to £1.5 million

- 12% above £1.5 million

Worked example: on a £270,000 home, you'd pay nothing on the first £125,000, then 2% on the next £125,000 (£2,500), then 5% on the final £20,000 (£1,000) — a total of £3,500.

First-time buyers (England & Northern Ireland):

- 0% up to £300,000

- 5% on the portion from £300,001 to £500,000

- No relief at all above £500,000 — standard rates apply to the whole price

So a first-time buyer purchasing that same £270,000 home pays £0 in stamp duty. Buy at £350,000 and you'd pay £2,500. One catch: if you're buying jointly, both of you must be first-time buyers to qualify.

Buying in Wales or Scotland? Different taxes apply. Wales charges Land Transaction Tax (LTT) with a 0% band up to £225,000 and no first-time buyer relief; Scotland's Land and Buildings Transaction Tax (LBTT) starts at £145,000, or £175,000 for first-time buyers.

Second homes and buy-to-lets attract a 5% surcharge on every band in England - a £300,000 second home means around £20,000 in stamp duty.

Stamp duty is due within 14 days of completion and can't be added to a standard mortgage.

3. Solicitor and conveyancing fees

You can't legally buy a home in the UK without conveyancing, the legal work of transferring ownership. Expect to pay £800–£2,000 depending on the property price, whether it's leasehold (more complex, so pricier), and whether you use a local solicitor or an online conveyancer.

Watch out for the extras that sit on top of the headline quote:

- Searches (local authority, environmental, drainage and water): £250–£450

- Land Registry fee: £150–£330 depending on price

- Bank transfer fees: £20–£50

- Leasehold supplements: often £200–£500 extra

A realistic all-in conveyancing budget for a freehold purchase is £1,200–£1,800. Get an itemised quote up front and check whether it's "no completion, no fee" - worth having if your purchase falls through, which happens to roughly one in three UK transactions.

4. The survey: the cost buyers most want to skip (and shouldn't)

Here's the uncomfortable truth: your lender's mortgage valuation is not a survey. It exists to protect the bank's money, not yours - it often involves nothing more than a drive-by or a desktop check.

If you want to know what you're actually buying, you need your own survey:

- RICS Level 2 (HomeBuyer Report): £400–£800. Suitable for conventional properties in reasonable condition. Flags visible issues like damp, roof problems and structural movement.

- RICS Level 3 (Building Survey): £700–£1,500+. The comprehensive option — essential for older properties, anything unusual, or homes that have been significantly altered.

It's tempting to see £600 as an optional saving when you're already stretched. It isn't. Surveys routinely uncover issues costing thousands, a failing roof alone can cost thousands to replace and a survey finding is your strongest negotiating tool. Knock £5,000 off the price because of a damp problem, and your survey just paid for itself eight times over.

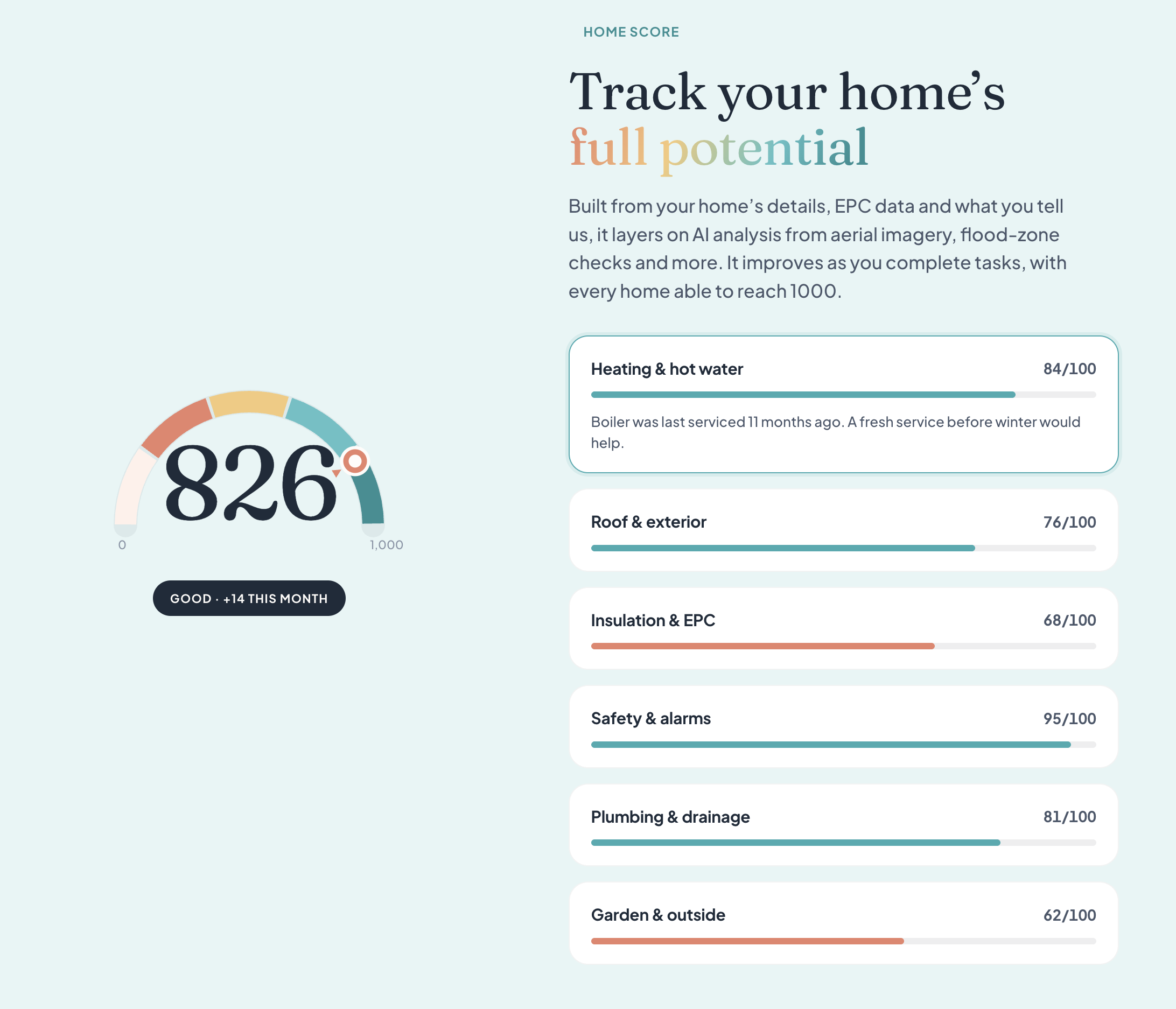

Savvy buyers are also doing digital due diligence before they get to survey stage. Tools like Planna's HomeScore assess a property's Safety, Condition and Energy profile across 1,000 data points, and RoofScore analyses roof condition from aerial imagery - for a fraction of a survey's cost. That doesn't replace a survey, but it tells you which properties are worth pursuing (and surveying) in the first place, and arms you with questions before you offer.

5. Mortgage fees

Often forgotten in budgeting, mortgage costs can add up to £1,500+:

- Arrangement/product fee: £0–£1,500. Many of the best rates carry a fee of around £999. It can usually be added to the loan, but you'll then pay interest on it for 25+ years - pay upfront if you can.

- Valuation fee: £0 - £400. Many lenders now include a free basic valuation.

- Broker fee: £0 - £999. Plenty of good brokers are free to you (paid by the lender); others charge a fixed fee.

- Telegraphic transfer fee: £25 - £50.

6. The costs nobody budgets for

- Removals: £400–£1,500 depending on distance and how much stuff you own. A van-and-mates move might cost £150; a full-service move across the country can top £2,000.

- Buildings insurance: required from exchange (not completion) - typically £150 - £400 a year.

- Immediate repairs and essentials: budget at least £500–£1,000 for locks (always change them), basic fixes, and the things the survey told you about.

- Furniture and appliances: if the sellers take the white goods, a cooker, fridge-freezer and washing machine will set you back £1,000+ before you've bought a sofa.

Putting it all together: three worked examples

First-time buyer, £270,000 home, 10% deposit (England): Deposit £27,000 + stamp duty £0 + conveyancing £1,400 + Level 2 survey £550 + mortgage fees £1,000 + moving costs £800 = ~£30,750 upfront

Home mover, £350,000 home, 15% deposit (England): Deposit £52,500 + stamp duty £7,500 + conveyancing £1,600 + Level 3 survey £1,100 + mortgage fees £1,000 + moving costs £1,200 = ~£64,900 upfront

First-time buyer, £212,000 home, 5% deposit (Wales): Deposit £10,600 + LTT £0 + conveyancing £1,300 + Level 2 survey £500 + mortgage fees £800 + moving costs £600 = ~£13,800 upfront

How to keep costs down (without cutting corners)

- Time your purchase around thresholds. In England, a first-time buyer purchase at £300,000 attracts zero stamp duty; at £310,000 it costs £500. Around key thresholds, small negotiations have outsized effects.

- Shop the conveyancing quote. Fees for identical work vary by hundreds of pounds. Get three quotes, compare the full itemised cost, and check reviews, the cheapest quote with terrible communication can cost you the purchase.

- Don't skip the survey - target it. Use pre-offer research to understand a property's likely condition risks, then choose the right survey level rather than defaulting to the cheapest.

- Negotiate with evidence. Every issue you find before exchange is a pound off the price or a repair the seller funds. After completion, it's your bill.

- Keep a buffer. Aim to complete with at least £2,000–£3,000 still in the bank. The first month in a new home always costs more than you think.

The bottom line

Buying the average UK home in 2026 costs roughly £30,000–£37,000 upfront for a typical buyer with a 10% deposit and the further above average you buy, the faster the non-deposit costs stack up. The deposit gets all the attention, but it's the £5,000–£10,000 of "other" costs that catch buyers out, because almost all of it must be paid in cash.

The single best defence is information: know your stamp duty bill before you offer, know the property's condition before you fall in love with it, and know your total number, not just your deposi.

Get a free HomeScore for any UK property via our app and see its Safety, Condition and Energy profile in minutes. You can check out the property report here